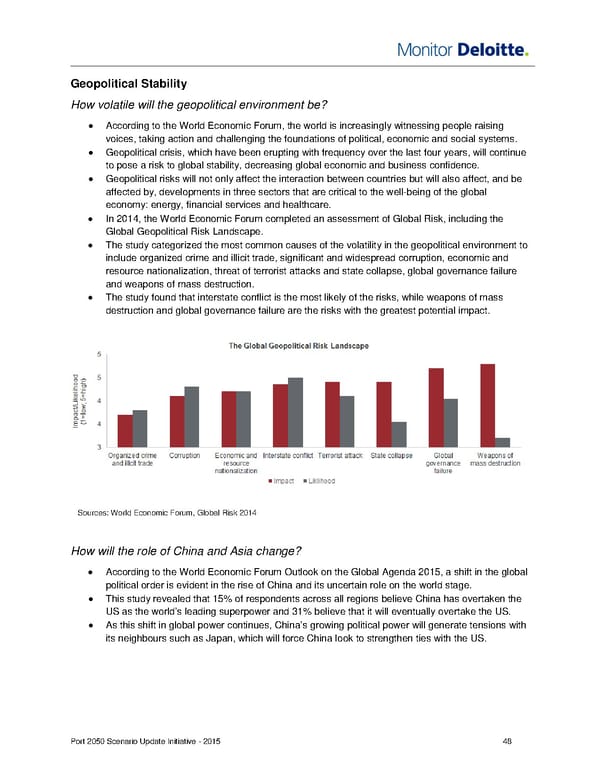

Geopolitical Stability How volatile will the geopolitical environment be? • According to the World Economic Forum, the world is increasingly witnessing people raising voices, taking action and challenging the foundations of political, economic and social systems. • Geopolitical crisis, which have been erupting with frequency over the last four years, will continue to pose a risk to global stability, decreasing global economic and business confidence. • Geopolitical risks will not only affect the interaction between countries but will also affect, and be affected by, developments in three sectors that are critical to the well-being of the global economy: energy, financial services and healthcare. • In 2014, the World Economic Forum completed an assessment of Global Risk, including the Global Geopolitical Risk Landscape. • The study categorized the most common causes of the volatility in the geopolitical environment to include organized crime and illicit trade, significant and widespread corruption, economic and resource nationalization, threat of terrorist attacks and state collapse, global governance failure and weapons of mass destruction. • The study found that interstate conflict is the most likely of the risks, while weapons of mass destruction and global governance failure are the risks with the greatest potential impact. Sources: World Economic Forum, Global Risk 2014 How will the role of China and Asia change? • According to the World Economic Forum Outlook on the Global Agenda 2015, a shift in the global political order is evident in the rise of China and its uncertain role on the world stage. • This study revealed that 15% of respondents across all regions believe China has overtaken the US as the world’s leading superpower and 31% believe that it will eventually overtake the US. • As this shift in global power continues, China’s growing political power will generate tensions with its neighbours such as Japan, which will force China look to strengthen ties with the US. Port 2050 Scenario Update Initiative - 2015 48

Monitor Deloitte - Final Report Page 49 Page 51

Monitor Deloitte - Final Report Page 49 Page 51